What to Watch as the Fed Meets Amid Bank Turmoil

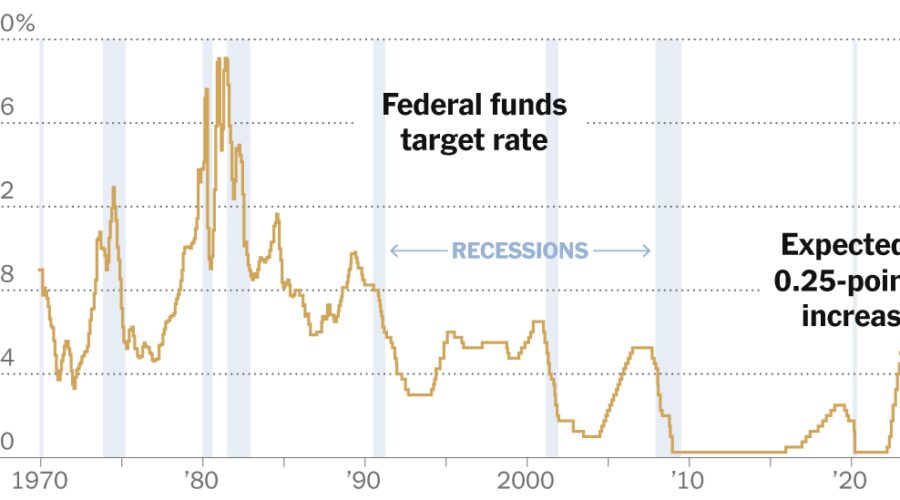

Just two weeks ago, Federal Reserve officials were hinting that they might consider a large, half-point rate increase at the conclusion of their meeting on Wednesday as the economy showed sustained momentum.

A series of bank failures since then have not only convinced investors and Wall Street economists that policymakers will lift borrowing costs by just a quarter-point on Wednesday — some are questioning whether central bankers will raise them at all.

Investors are most heavily betting on a quarter-point increase, but are penciling in a chance that the Fed will pause what has been a steady campaign to raise borrowing costs to contain rapid inflation. Goldman Sachs economists think it is likely that central bankers will hold off on a rate move this month, before resuming them in May.

This Fed decision carries enormously high stakes. If investors believe that central bankers are not sufficiently attuned to the turmoil gripping the banking industry, jittery markets could recoil. Yet if officials pause their rate increases to allow the tumult to pass, they could appear to be giving up on their fight against still-rapid inflation.

Jerome H. Powell, the Fed chair, will have a chance to explain both the Fed’s rate decision and its latest economic projections — which are scheduled for their first update since December — at a 2:30 p.m. Eastern news conference following the release of the decision and projections half an hour earlier. Mr. Powell may need to walk a fine line as he balances stubborn inflation with unfolding banking industry problems. Here’s what to watch, and why this meeting will be so fraught.

A rate increase could further squeeze banks.

The failure of Silicon Valley Bank on March 10 tied back partly to the Fed’s recent rate moves: The bank held a lot of long-term securities that had become less valuable as interest rates rose. Those losses helped to spook its depositors and spark a bank run that led to the bank’s collapse.

The question for the Fed is whether the bank’s demise is an isolated instance of a firm that did not plan well enough for rising borrowing costs, or a sign that the central bank’s fastest rate increases since the 1980s have pushed the financial system to a breaking point.

Inflation remains a big challenge.

The Fed is raising interest rates for a reason, though: Inflation is high, and it is not going away quickly. Consumer prices increased by 6 percent in the year through February, and while annual inflation has been slowing, monthly gains have recently sped back up. That bumpy progress has come just as the broader economy has proved more resilient than expected.

Strong momentum in prices and the labor market would usually spur more aggressive Fed rate moves, but bank upheaval is a complication: If smaller banks lend less amid the turmoil, that itself could slow the economy.

Rate projections could be key.

Given the uncertainty, the Fed’s economic projections could become a focal point. The central bank releases its forecasts once every three months, offering a snapshot of how officials expect unemployment, inflation and interest rates to evolve.

Fed officials had been widely expected to nudge up their forecasts for how high rates would rise by the end of 2023 — an estimate that stood at just above 5 percent in December. Whether that peak rate estimate will move in the latest projections is now much less certain.

Some economists — including Diane Swonk at KPMG — think that the Fed could scrap the economic projections altogether at this meeting, given the uncertain backdrop. But if they do give estimates, it will offer insight into how much of a beating officials expect the economy to take from the banking crisis. Economic estimates had to be submitted the Friday before the meeting, but officials could change them up until Tuesday night.

Source: Read Full Article